Last updated on Jul 1, 2026

IRS 8734 2004-2026 free printable template

pdfFiller is not affiliated with IRS

Fill out

Complete the form online in a simple drag-and-drop editor.

eSign

Add your legally binding signature or send the form for signing.

Share

Share the form via a link, letting anyone fill it out from any device.

Export

Download, print, email, or move the form to your cloud storage.

Why pdfFiller is the best tool for your documents and forms

End-to-end document management

From editing and signing to collaboration and tracking, pdfFiller has everything you need to get your documents done quickly and efficiently.

Accessible from anywhere

pdfFiller is fully cloud-based. This means you can edit, sign, and share documents from anywhere using your computer, smartphone, or tablet.

Secure and compliant

pdfFiller lets you securely manage documents following global laws like ESIGN, CCPA, and GDPR. It's also HIPAA and SOC 2 compliant.

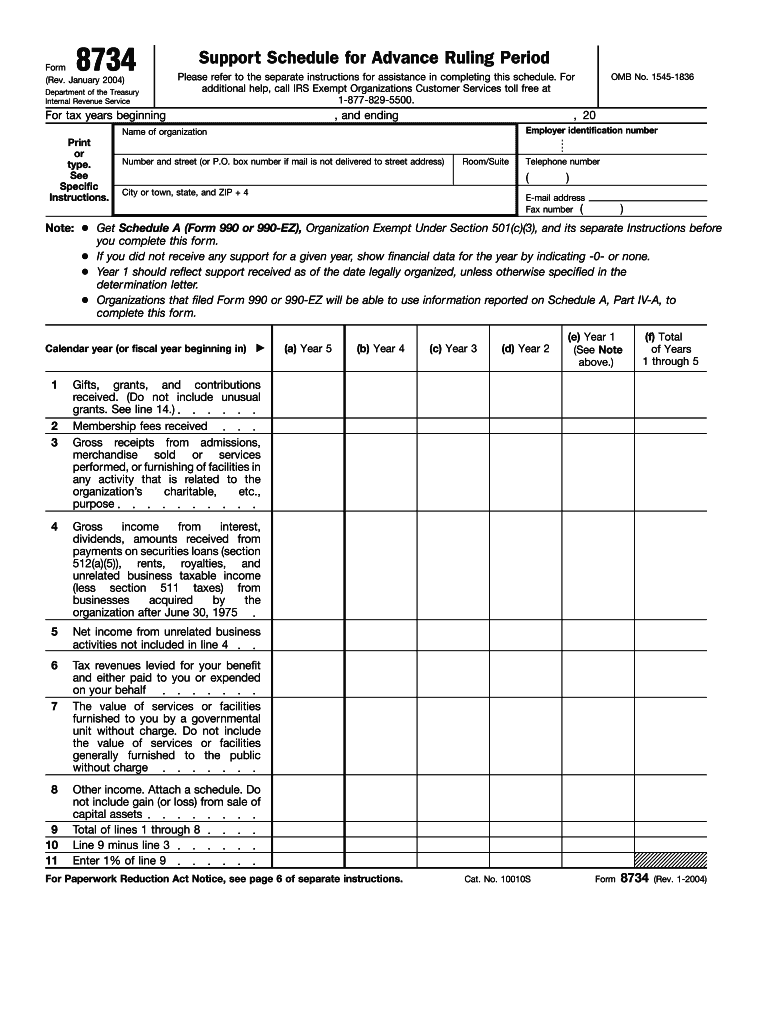

What is IRS 8734

The IRS Form 8734 Support Schedule is a federal tax form used by tax-exempt organizations to assess their public support percentage over designated tax years.

pdfFiller scores top ratings on review platforms

Who needs IRS 8734?

Explore how professionals across industries use pdfFiller.

IRS 8734 is needed by:

-

Nonprofit organizations assessing public support percentage

-

Tax-exempt entities required to report financial information

-

Trustees, officers, or directors responsible for financial reporting

-

Organizations applying for tax-exempt status

-

Entities receiving grants or public support

-

Tax professionals assisting clients with tax-exempt organizations

Comprehensive Guide to IRS 8734

What is IRS Form 8734 Support Schedule?

IRS Form 8734 is a crucial document for tax-exempt organizations, serving the purpose of determining public support percentages. This support schedule form helps organizations comply with the public support test, which is essential for maintaining tax-exempt status. The form requires the reporting of detailed financial data, including various income sources such as gifts, grants, and contributions. It is mandatory for an authorized officer, director, or trustee to sign the form to validate its accuracy.

Purpose and Benefits of IRS Form 8734 Support Schedule

The IRS Form 8734 plays a significant role in the financial reporting processes of tax-exempt entities. By accurately filling out this form, organizations can determine their levels of public support, which directly affects their funding capabilities. Compliance with IRS regulations is another essential reason for completing the form, as it preserves an organization's tax-exempt status and avoids potential penalties. Notably, transparent reporting of financial data can also enhance opportunities for future funding.

Who Needs to Complete IRS Form 8734 Support Schedule?

Several types of tax-exempt organizations are required to complete IRS Form 8734. This includes charities and nonprofits that rely on public donations and support. Understanding the eligibility criteria is critical; organizations must ensure they are compliant with both federal and state-specific rules regarding filing this form. Familiarity with these requirements helps prevent any missteps that could jeopardize their tax-exempt status.

How to Fill Out the IRS Form 8734 Support Schedule Online

Filling out the IRS Form 8734 online is a straightforward process. Here are the steps to follow:

-

Access the fillable form on a reliable platform.

-

Enter essential details such as the organization's name and Employer Identification Number (EIN).

-

Complete each field as per the guidelines provided.

-

Review your entries for accuracy to prevent errors.

-

Sign the document electronically if required.

Taking these precautions can help avoid common mistakes that might delay processing.

Field-by-Field Instructions for IRS Form 8734 Support Schedule

Each section of the IRS Form 8734 requires specific information. Below is a breakdown of essential fields and the information needed:

-

Organization Name: Provide the legal name of the nonprofit.

-

Employer Identification Number (EIN): Essential for identifying the organization.

-

Public Support Test Percentage: Calculate this accurately for determining compliance.

Organizations should be aware of common errors in these sections, such as incorrect EINs or mismatched names, as these could lead to rejections during processing. Ensuring accuracy is paramount.

Submission and Filing Methods for IRS Form 8734 Support Schedule

Submitting the completed IRS Form 8734 can be done through various methods. Organizations can choose to file online or send a paper copy via mail. Important deadlines must be observed to prevent penalties:

-

Online submission through a designated platform is often preferred for speed.

-

Mailing details should be verified to avoid lost documents.

-

Be aware of filing deadlines to ensure timely compliance.

Late or incorrect submissions may lead to significant complications, including potential audits.

Post-Submission Process for IRS Form 8734 Support Schedule

After the IRS Form 8734 is submitted, organizations can expect to receive a confirmation receipt. The processing times vary; however, following the submission, organizations should:

-

Keep the confirmation for record-keeping purposes.

-

Check the application status periodically.

-

Know common rejection reasons to address any issues promptly.

Being proactive in these steps can mitigate concerns regarding the application process.

Security and Compliance for IRS Form 8734 Support Schedule

When handling sensitive documents like the IRS Form 8734, data security and compliance are of utmost importance. Platforms like pdfFiller employ 256-bit encryption and adhere to security standards such as SOC 2 Type II and HIPAA regulations. Protecting data during tax filings is vital to prevent unauthorized access and maintain compliance with IRS guidelines, ensuring that organizations are prepared for potential audits.

How pdfFiller Supports Your IRS Form 8734 Needs

pdfFiller offers robust features for organizations navigating their IRS Form 8734 requirements. Users can easily create, fill, and sign the form online with security measures in place for document management. Utilizing pdfFiller simplifies the complexities involved in tax form submissions, allowing organizations to focus on their missions without worrying about the administrative burden.

Example of a Completed IRS Form 8734 Support Schedule

For a clear understanding of how to properly fill out the IRS Form 8734, an annotated example is useful. This example will illustrate each section and include explanations relevant to specific entries:

-

Each filled field corresponds to specific requirements outlined in the form.

-

Annotations against sections can illustrate common pitfalls to avoid.

Utilizing an example can serve as a valuable reference when preparing the form.

How to fill out the IRS 8734

-

1.To access and open the IRS Form 8734 Support Schedule on pdfFiller, navigate to the pdfFiller website and use the search bar to find the form by typing 'IRS Form 8734'.

-

2.Once you find the form, click on it to open the interactive PDF editor. Here, you will see fillable fields that you can fill out directly on screen.

-

3.Before you start filling out the form, gather all necessary financial data, including your organization’s gifts, grants, contributions, and other income sources, as you will need this information to complete the form accurately.

-

4.As you fill in the form, click on each blank field to enter your organization’s name, Employer Identification Number, and financial details. Use pdfFiller's tools to add text and checkboxes as needed.

-

5.If you make errors or need to revise, pdfFiller allows you to easily delete or adjust your entries. Make sure to double-check all information before proceeding.

-

6.After completing all sections of the form, review your entries carefully. Ensure all required fields are filled correctly and the document is ready for signature.

-

7.Once satisfied with the filled form, save your work. You can download it as a PDF or choose to submit directly through pdfFiller if required.

Who needs to file IRS Form 8734?

IRS Form 8734 is required for tax-exempt organizations that need to report their financial data for the public support test. This includes nonprofits and entities responsible for overseeing their organization's finances.

What information is required to complete IRS Form 8734?

To complete the form, you need financial details such as gifts, grants, contributions, and other income sources, as well as your organization's name and Employer Identification Number.

What are the submission methods for IRS Form 8734?

Form 8734 can typically be submitted electronically if required or mailed to the IRS. Always verify specific submission instructions based on current IRS guidelines.

What are common mistakes when filing Form 8734?

Common mistakes include incomplete fields, inaccurate financial data, and forgetting to sign the document. Double-check all entries to avoid delays or rejections.

What is the deadline for filing IRS Form 8734?

The deadline for submitting Form 8734 usually aligns with your organization’s tax return due date. Check IRS guidelines for the specific year to ensure timely compliance.

Are there any fees associated with filing IRS Form 8734?

There are generally no fees for submitting IRS Form 8734 unless you hire a tax professional for assistance. However, be aware of potential fees if filing late.

What is the purpose of IRS Form 8734?

The purpose of IRS Form 8734 is to assess the public support percentage of tax-exempt organizations, ensuring compliance with IRS regulations regarding public support tests.

Related Content

Related Forms

Related Catalogs

Get the latest insights from our blog

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

This form may include fields for payment information. Data entered in these fields is not covered by PCI DSS compliance.